For sophisticated commercial real estate investors, securing the right financing is as critical as acquiring the right asset. The capital structure of a deal dictates everything from cash flow and returns to the level of risk exposure. Two of the most prominent sources of debt capital are traditional banks and government-sponsored enterprises (GSEs), commonly known as agency lenders. This guide is designed for experienced investors and developers to dissect the nuances of bank vs agency financing, helping you align your capital strategy with your investment objectives.

You will learn the key differentiators between these financing options, including their impact on interest rates, flexibility, and risk. Understanding this landscape is fundamental to optimizing your portfolio and making strategic financing decisions that propel your growth.

Understanding the Core Players: Banks vs. Agencies

At first glance, a loan is a loan. However, the source of that capital dramatically alters its terms, structure, and suitability for a given project. Think of it like choosing a vehicle for a cross-country race. A sports car might be faster on a straightaway, but a rugged off-road truck is better prepared for unpredictable terrain. Similarly, bank and agency loans are engineered for different purposes and market conditions.

Bank Financing

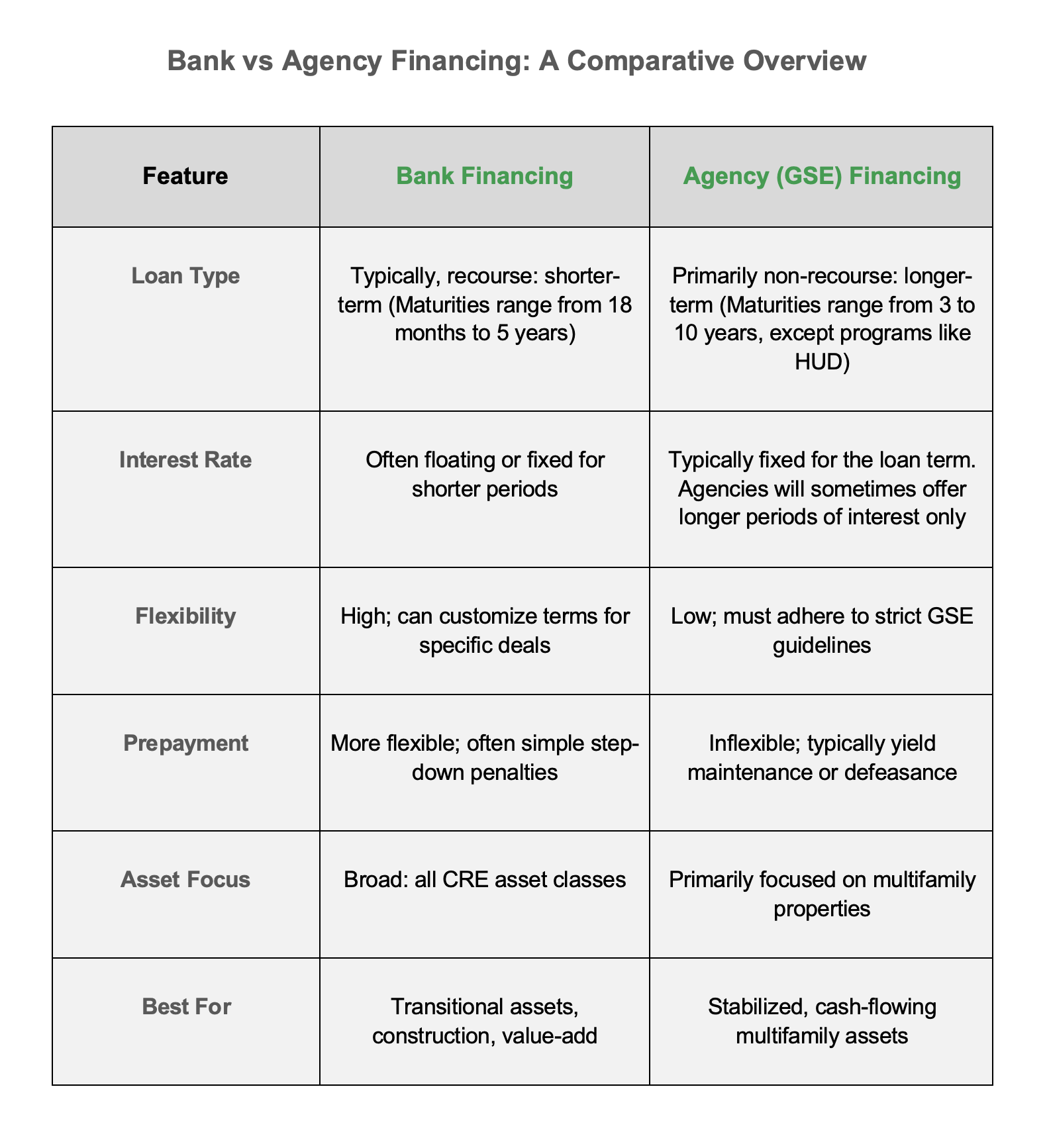

Originates from depository institutions like commercial banks, community banks, and credit unions. Their primary business is taking deposits and making loans. As portfolio lenders, they typically hold the loans they originate on their own balance sheets. This gives them significant discretion over underwriting and loan terms, but it also means their risk appetite can fluctuate with economic cycles and regulatory pressures.

Agency Financing

Provided by lenders who originate loans on behalf of government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. These agencies don’t lend directly to borrowers. Instead, they purchase qualifying loans from approved lenders, package them into mortgage-backed securities (MBS), and sell them to investors on the secondary market. This model provides a consistent and liquid source of capital for the multifamily housing market, but it requires strict adherence to standardized underwriting criteria.

Key Benefits and Strategic Use Cases of Bank vs Agency Financing

Choosing between bank and agency financing depends entirely on the asset’s profile and your investment strategy. One is not inherently better than the other; they are simply different tools for different jobs.

When Bank Financing Excels in CRE

Bank loans are the preferred choice for investors seeking flexibility and creative structuring. Their ability to underwrite deals on a case-by-case basis makes them ideal for assets that don’t fit neatly into a standardized box.

- Value-Add and Transitional Properties: Banks are more comfortable financing properties that require repositioning, renovation, or lease-up. They can underwrite based on a future stabilized value and may offer interest-only periods to accommodate the business plan.

- Construction and Development: For ground-up construction or significant redevelopment projects, banks are the primary source of capital, offering construction loans that fund in draws as the project progresses. Banks are also more likely to offer interest only periods on transitioning assets or assets under development.

- Diverse Asset Classes: While agencies focus almost exclusively on multifamily, banks will lend on office, retail, industrial, hospitality, and specialty properties.

- Relationship-Driven Lending: A strong, established relationship with a bank can lead to more favorable terms and a smoother process, as the lender has familiarity with your track record and financial strength.

The trade-off for this flexibility is often a personal guarantee. Most bank loans are recourse, meaning the lender can pursue your personal assets if the property’s sale doesn’t cover the loan balance. They also tend to be shorter-term, creating future refinance risk.

When Agency Financing Is the Optimal Choice in CRE

Agency financing is the gold standard for long-term, stable acquisitions of multifamily properties. If your goal is to lock in favorable terms and minimize personal risk on a cash-flowing asset, an agency loan is often the superior option.

- Long-Term Fixed Rates: Agency lenders offer long-term fixed-rate debt (up to 30 years), which eliminates interest rate risk for the life of the hold period. This predictability is invaluable for long-term investors.

- Non-Recourse Structure: This is a major advantage. In a non-recourse arrangement, the borrower is not personally liable for the loan beyond the pledged collateral. Liability occurring in specific “bad boy” acts, such as fraud, gross negligence, or willful misconduct, as defined in the carve-out guaranty. Outside of these exceptions, a default on the loan does not trigger recourse to the borrower’s other assets or properties, thereby isolating risk and preserving the integrity of the broader portfolio.

- Higher Leverage & Amortization: Both banks and agency lenders commonly offer 25- or 30-year amortization schedules, depending on the borrower’s profile and the deal structure. However, agency lenders may offer longer interest-only periods, particularly for stabilized assets or low-leverage transactions, making them attractive for maximizing early cash flow.

- Capital Availability: Because agency loans are fueled by the secondary market, they provide a consistent source of liquidity that is less susceptible to regional economic downturns than bank lending.

- Relationship-Driven: Agency lenders do place strong emphasis on the underlying asset’s performance, but they also consider the borrower’s track record and existing relationships, especially for repeat sponsors or those with strong portfolios.

The primary limitations are a lack of flexibility and significant prepayment penalties. Agency underwriting is rigid, and the property must meet specific criteria related to occupancy, debt service coverage, and physical condition. Early prepayment is costly, making these loans unsuitable for short-term holds.

A Step-by-Step Guide to the Process to Financing

While the goal—securing a loan—is the same, the path to closing differs significantly between bank and agency lenders.

The Bank Financing Process (Simplified)

- Initial Discussion: The process starts with a conversation with a loan officer. You present the deal, your business plan, and your financial background.

- Statements & Term Sheet: Submit due diligence documents (rent roll, operating statements, personal financial statements, etc.). The bank process typically begins after reviewing operating statements and a current rent roll. While banks may give preliminary verbal indications once materials are received, they rarely issue formal commitment letters.

- Underwriting & Credit Committee: The loan officer and an underwriter will analyze the deal and prepare a credit memo. This package is then presented to an internal credit committee review. This is where the bank’s internal discretion plays a major role.

- Commitment & Closing: Once approved, the bank will inform you that the loan has been approved. From there, you move to documentation and closing.

The Agency Financing Process (Simplified)

- Sizing and Quoting: You work with an approved agency lender who “sizes” the deal based on GSE guidelines for LTV, DSCR, and net operating income. They will then provide a quote with an interest rate based on current MBS market pricing.

- Application & Deposit: You sign the application and provide a deposit to cover third-party reports (appraisal, property condition assessment, environmental report).

- GSE Underwriting: The lender underwrites the loan according to the strict standards set by Fannie Mae or Freddie Mac. The file is then submitted to the agency for their review and approval. The agency has the final say.

- Rate Lock & Closing: Once the GSE issues a commitment, you can lock your interest rate. The process then moves to documentation and closing.

Key Takeaways: Making the Right Decision

The choice between bank and agency financing is a strategic decision that should be driven by your specific goals for the asset.

- Recourse vs. Non-Recourse: Your tolerance for personal liability is a primary dividing line. Banks often require it; agencies offer non-recourse financing with the only liability coming in to play if certain fraudulent acts have occurred (a “carve-out” guaranty).

- Hold Period: If you plan to sell or refinance in 3-5 years, a bank loan with a flexible prepayment structure is likely a better fit. For a 10+ year hold, the long-term fixed rate of an agency loan is highly attractive.

- Asset Type & Condition: Is the property stabilized and cash-flowing, or does it require significant repositioning? Stabilized multifamily points to agency; value-add or non-multifamily assets point to banks.

- Interest Rate Outlook: In a rising rate environment, locking in a long-term fixed rate with an agency loan can be a powerful defensive move. In a falling rate environment, a shorter-term bank loan may allow you to refinance into better terms sooner.

How Essex Capital Markets Provides Clarity

Navigating the complexities of bank and agency financing options requires deep market knowledge and strong lender relationships. At Essex Capital Markets, we serve as your strategic capital advisor, providing the expertise to structure the optimal financing solution for your deal.

We go beyond simply quoting rates. We analyze your asset and business plan to determine which capital source aligns with your objectives. Our extensive network includes both relationship-driven banks and top-tier agency lenders across the country. This allows us to create a competitive environment and secure expert-driven solutions tailored to your needs, ensuring swift decision-making and a streamlined closing process.

Final Thoughts

Ultimately, the right financing strategy is not about finding the lowest interest rate; it’s about finding the structure that best supports your investment thesis while mitigating risk. Whether the flexibility of a bank loan or the security of an agency loan is the right choice, a deep understanding of both options is essential for any serious commercial real estate investor.

Frequently Asked Questions: Comparing Bank vs. Agency Loans for Commercial Real Estate Investors

What is the main difference between bank and agency loans for commercial real estate?

Bank loans are typically more flexible and suited for short-term, transitional, or value-add projects, while agency loans offer long-term, fixed-rate, non-recourse financing for stabilized multifamily properties.

When should I choose a bank loan over an agency loan?

Bank financing is ideal for projects needing flexibility, such as construction, repositioning, or non-multifamily asset classes like office, retail, or industrial. They’re also preferable for shorter hold periods and investors comfortable with recourse.

When is agency financing the best option?

Agency loans are best for long-term holds of stabilized multifamily properties where you want fixed rates, non-recourse terms, and maximum leverage. They offer consistent capital but have stricter underwriting guidelines and significant prepayment penalties.

-

Are agency loans always non-recourse?

Yes, agency loans are generally non-recourse, meaning your liability is limited to the property itself. However, “bad boy” carve-outs can still apply in cases of fraud or misrepresentation.

-

Can I use agency financing for commercial properties that are not multifamily?

No, agency loans from Fannie Mae and Freddie Mac are primarily intended for multifamily assets. For retail, office, hospitality, or industrial properties, bank financing is the more suitable option.

-

How do interest rates compare between bank and agency loans?

Agency loans usually offer long-term fixed interest rates, making them attractive in rising rate environments. Bank loans may have floating or shorter-term fixed rates, offering flexibility in a declining rate environment.

-

What are the prepayment penalties for bank vs. agency loans?

Bank loans typically have more lenient prepayment terms like step-down penalties. Agency loans often use yield maintenance or defeasance, which can be costly if you plan to exit early.

-

How long does it take to close a bank loan vs. an agency loans?

Bank loans can close more quickly due to less standardized underwriting. Agency loans, while highly structured, may take longer due to GSE approval and required third-party reports. Essex Capital Markets helps streamline both processes.

-

Is a personal guarantee required for bank loans?

Most bank loans are recourse, meaning the borrower may be personally liable if the property’s value doesn’t cover the debt. In contrast, agency loans are non-recourse, offering greater protection to the borrower.

-

How can a capital advisor like Essex Capital Markets help me choose the right loan?

Essex Capital Markets evaluates your asset, investment strategy, and financial profile to match you with the ideal lender—whether that’s a relationship-driven bank or a top-tier agency lender—ensuring the best possible structure for your deal.

About Essex Capital Markets

Essex Capital Markets, LLC offers bespoke financing solutions and multifamily advisory services to mid-market investors and developers. The team specializes in structuring tailored debt strategies, navigating complex transactions, and delivering certainty of execution across Chicago’s most competitive real estate submarkets.

Ready to explore the optimal financing strategy for your next acquisition or refinance? Let us help you unlock your capital potential. To speak with our Capital Markets team, please fill out the form below.